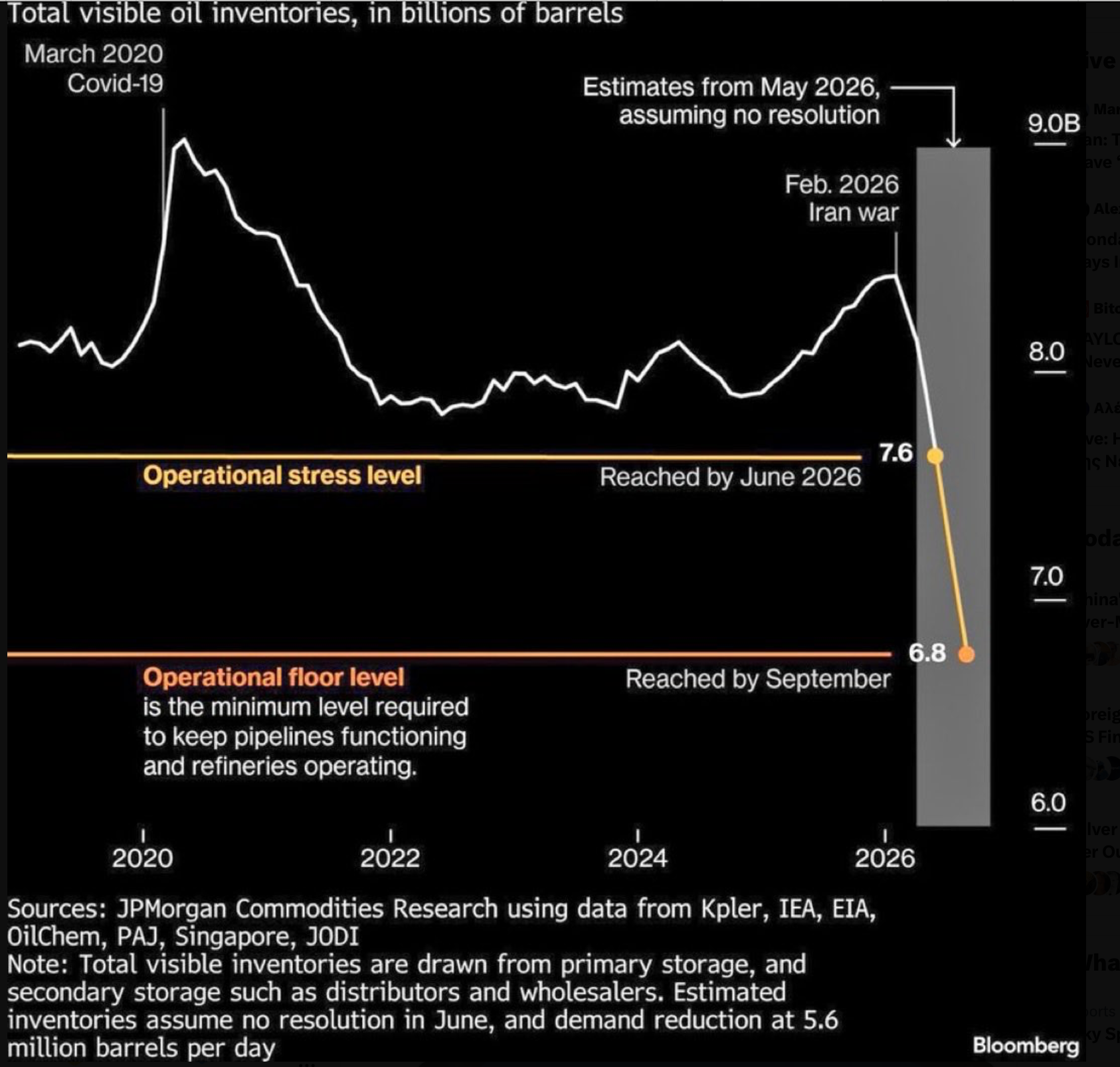

Earlier this week my colleagues and I spent some time discussing a pretty worrying JP Morgan chart, published as part of a wider Bloomberg article. It shows total visible oil inventories, measured in billions of barrels, but the picture it paints is one of an uncomfortable truth.

As the Bloomberg article recalls, oil inventories surged during Covid, when demand collapsed and the world suddenly had more oil than it knew what to do with. They were then steadily drawn down as economies reopened and energy demand returned. More recently, demand hasn’t fallen but supply chains are coming apart. The chart shows that as a result of this, inventories are falling sharply again as the Iran war disrupts flows from the Persian Gulf and leaves the Strait of Hormuz close to closure.

The warning from JP Morgan is that OECD oil inventories could hit operational stress levels in June and reach the operational minimum by September if the Strait of Hormuz does not reopen. Once inventories fall close to those minimum levels, prices may need to rise sharply enough to destroy demand. In plain English, that means higher costs for transport, aviation, manufacturing, agriculture, shipping and consumers.

Scary stuff indeed. But the chart is really about something larger than oil stocks, it is about the reassuring buffers that oil stocks offer the economy.

Modern economies have not grown to the size they are because they are perfectly designed or perfectly balanced. They work because they have cushions built into them. Most of the time, these buffers are invisible. Governments and companies do not usually shout about spare capacity, extra inventory or emergency reserves, partly because we have been encouraged to see buffers as inefficiencies, and partly because admitting the need for them rather ruins the impression that everything is permanently under control.

For decades, we have been told that the modern world would work better if it ran on just-in-time supply chains, globalised production, lean balance sheets, cheap energy, cheap money and the wonderful sponsored-by-Disney assumption that nothing serious would go wrong in more than one place at once.

And now reality has hit. Bloomberg reports that the world has been burning through oil inventories at record speed as the Iran war throttles flows from the Persian Gulf. Bloomberg cites Morgan Stanley estimates showing that global oil stockpiles fell by around 4.8 million barrels per day between the beginning of March and late April.

The immediate temptation is to ask one another, ‘how much oil is left?’. But the better question is, ‘how much oil is still usable before the system itself begins to malfunction?’.

Oil inventories are not like coins in a jar, where the last coin is just as useful as the first. The global oil system has an operational minimum. Like a car engine, it needs a certain amount of oil in order for it to stay in working order. Pipelines need a minimum flow and refineries need feedstock. Storage tanks, export terminals and distribution networks need working volumes. We should not only be asking whether the world is going to technically run out of oil. We should also be asking whether parts of the system are soon going to seize up.

JPMorgan’s Natasha Kaneva explained to Bloomberg: inventories are the shock absorber of the global oil system, but not every barrel can be drawn. The JP Morgan chart marks an operational stress level at around 7.6 billion barrels, and an operational floor at around 6.8 billion barrels. The stress level is where the system begins to creak, while the floor is the minimum level required to keep pipelines functioning and refineries operating.

This is of course pointing to a common point so many of us in the gold and silver world are all too familiar with: the modern economy is still physical. For all the talk of artificial intelligence, digital payments and cloud computing, the real economy still runs on real commodities. In this case we’re talking about oil, diesel, jet fuel, shipping, plastics, chemicals, fertiliser, mining, construction and functioning logistics. Oil is embedded in food production, aviation, freight, manufacturing, medicine, packaging and military supply chains. It is everything, everywhere and all at once.

So pernicious is it that when oil inventories fall towards critical levels, the effect isn’t confined to one commodity market. It moves through the bloodstream of the entire economy.

This is the problem with systems that are optimised for efficiency rather than resilience. They look superb in normal times because they produce lower costs, higher returns and prettier spreadsheets, but they also hide fragility until the moment it matters. A system with no buffer may look stronger than everyone else’s on a calm day, but when the shock arrives it has nowhere to absorb the blow.

That lesson applies far beyond oil. Banks fail when confidence breaks and liquidity falls below the level needed to keep the system functioning. Supply chains fail when the buffer disappears. Currencies do not collapse because every note suddenly becomes worthless. They lose credibility gradually, and then the process becomes impossible to ignore and everything comes to an end very quickly indeed.

The world does not need to run out of oil for the system to become unstable. It only needs to fall below the level at which the machinery of supply can function smoothly. That is true of oil, but it is also true of banking, supply chains, currencies and trust.

Buy Gold Coins

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here.

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here