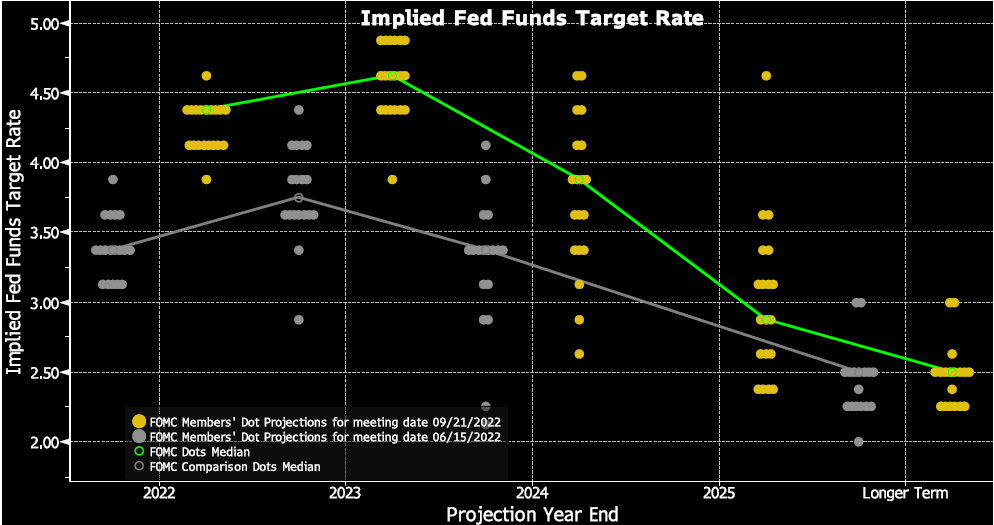

Fed’s message this week – higher rates, lower economic growth, higher unemployment. The Fed hiked interest rates by 75 basis points for the third straight meeting and the statement said that the committee anticipates further increases.

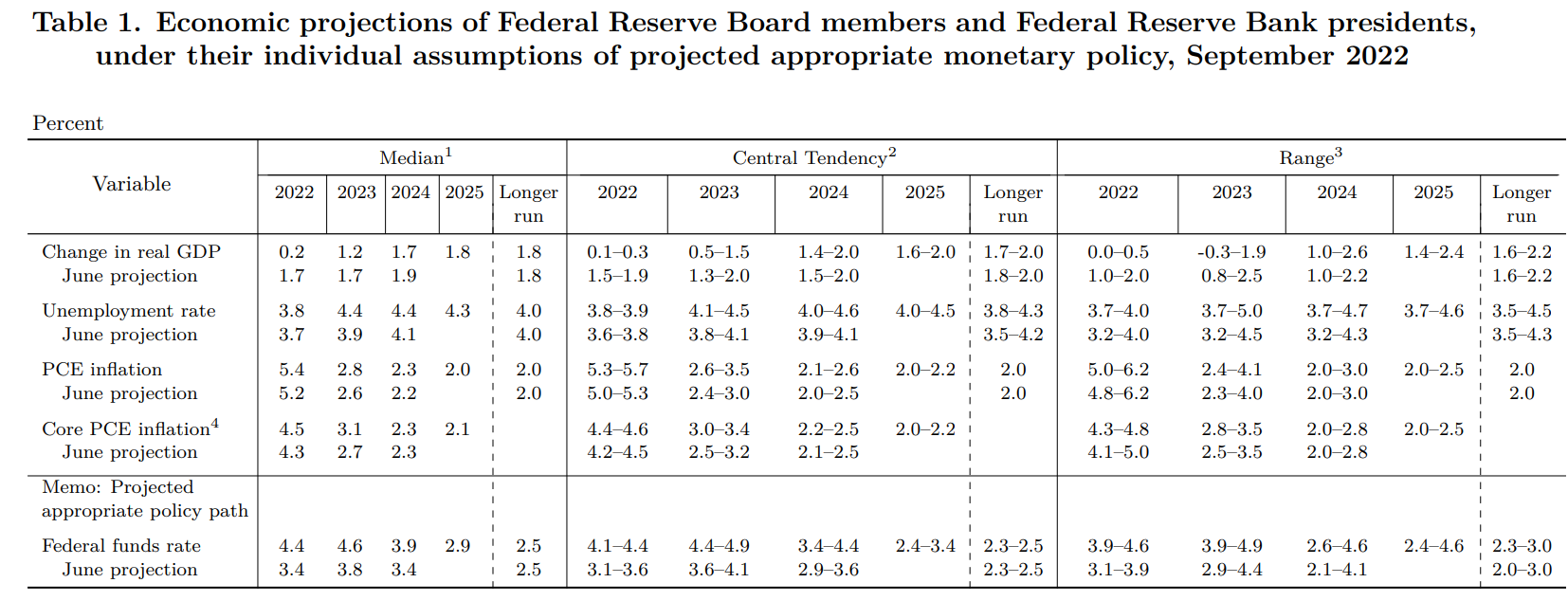

The Summary of Economic Projections (SEP) showed that the median projection is for a further 1.25% increase by yearend.

Another 75 basis points at the November 1-2 meeting and 50 basis points at the December 13-14 meeting. The projections then show a further 25 basis point increase next year before the Fed holds then starts to lower rates in 2024.

Central Banks Have Already Lost Control Over the Markets

The statement did acknowledge that Russia’s war against Ukraine is causing tremendous human and economic hardship.

The war and related events are creating additional upward pressure on inflation and are weighing on global economic activity. The Committee is highly attentive to inflation risks.

The difficulty is that central banks have zero control over supply issues and their only response is to choke demand to meet the limited supply.

Also, the approach of raising interest rates does not target sectors but is instead broad based across the entire economy.

Download Your Free Guide

Although financial markets react to interest rate increases very quickly, and many times are forward looking, i.e. equity markets decline before a rate increase, it takes 6 to 12 months for the full effects of interest rate increases to reach the broad based economy.

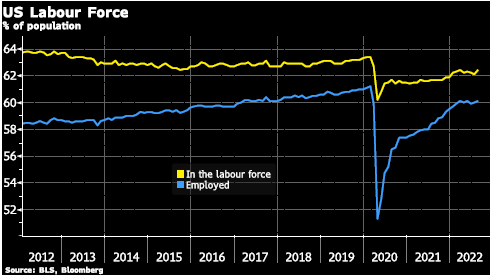

Lies, damned Lies, and statistics – statistics can be misleading. The U.S. unemployment rate is one of the main indicators the Fed uses for its measure of the labour market.

The caveat is that a person without a job must have actively looked for a job in the last four weeks to be counted as unemployed. Otherwise, they are not counted as a participant in the labour force.

In other words, because of the way the unemployment rate is calculated it could be ‘artificially low’.

What we can Learn from the International Gold Market

Watch Jan Niewenhuijs Only on GoldCore TV

People are ‘dropped out of the labour force figures’ instead of being counted as unemployed.

The percent of the population in the labour force has not recovered to pre-covid levels – i.e. there are fewer people in the labour force.

The number of employed in the U.S. as a percent of the population has also not recovered to pre-covid levels. So it may turn out that the FED believes employment markets are stronger than they actually are because of misleading statistics.

And since the FED wants to raise interest rates until the labour market breaks, maybe they are raising rates based on bad statistics.

The Blame Game Continues…

There are many reasons quoted by individuals for not returning to the labour market. The highest job openings brackets are in health care and hospitality.

The burnout rate during/post covid of healthcare workers has many moving to different sectors or choosing to advance their education, stay home, or early retirement instead of returning to the sector.

The high burnout of healthcare workers coupled with an average salary of US$48,000 to $65,000 for a paramedic in New York City, where the monthly average rent is close to $4,000.

It is no wonder there are more job openings than applicants in this sector. Wage inequality has been a very long-standing problem in the U.S. According to Forbes the average S&P 500 CEO currently makes 299 times the average employee.

This compares to the average CEO earning 50 times more than the average employee in 1950. In the current post-covid, the high inflationary environment is ripe for U.S. employees to demand higher wages.

The Fed wants to lower demand by getting higher income households and businesses to slow their spending without pushing lower income households even further down the poverty rabbit hole.

Powell is quick to point out that it is lower income households that are the most negatively affected by inflation, but it is also lower income households that are the most negatively affected by higher interest rates. Also, lower income households are even more affected by high unemployment levels.

Jim Rogers Interview Only on GoldCore TV

The SEP projections also show that the Fed does expect economic growth to be weaker than its June Projection (table below) with only 0.2 growth this year and 1.2% growth next year.

With a higher unemployment rate projected at 4.4%, this implies more than 1 million additional unemployed people in America. And still, inflation is well above the Fed’s 2% target.

High inflation, and rising unemployment have strong parallels to the early 1980s. Add to this a U.S. Administration that blames everyone but themselves for the issues at hand…we are reminded of Jimmy Carter.

The Fed was late to recognize inflation, late to raise rates, and late to start quantitative tightening (shrinking the balance sheet), are they now going to be late to recognize how much effect the higher interest rates are slowing economic growth.

And if the two quarters of negative U.S. economic growth in the first half of the year and the disastrous earnings announcement from FedEx are any indications; not only the U.S. but the global slowdown is at hand!

When economic growth does slow politicians will turn the blame on central banks.

From The Trading Desk

Market Update

US interest rates rose by an expected 75bp yesterday.

Equity markets whipped back and forth in the afternoon session, initially falling then clawing back to flat on the day before selling off into the close as we got a much more hawkish Fed than expected.

The Dow Jones closed down 1.7% at 30,183 with the S&P down a similar % amount.

Equity markets look like they are close to giving back all their gains since the summer lows in June.

The dollar continues to strengthen with the Euro hitting a 20-year low.

The Bank of Japan this morning has just stepped in to prop up the Yen after a 26% fall this year against the USD.

This is the first time the BOJ has intervened in the FX market since 1998.

Given the strength of the USD and the higher treasury yields, Gold has held up reasonably well.

If you look at Gold in Euro and GBP terms, gold is actually up on the year. In Euro terms close to 6% and in GBP 10%.

Agree we are lower in USD but strip out the dollar strength component and gold in USD terms is down 5% on the year, compare this to the leading equity indices which are down over 20%.

Stock Update

Gold Britannia for immediate settlement – We have a limited number of Gold Brittania’s available for storage or immediate delivery at Spot plus 9.5%.

Gold Brittania’s on allocation – Due to the passing of Queen Elizabeth II, the production of new British gold and silver coins by the Royal mint is affected. Orders can still be placed on a back order/allocation basis.

We expect the order to start settling in 3 months’ time.

The premium for backorder/allocation Gold Brittania’s is Spot plus 6.5%

GoldCore have excellent stock and availability on all gold coins and bars.

Please contact our trading desk with any questions you may have.

Silver coins are now available for delivery or storage in Ireland and the EU with the lowest premium in the market.

Starting as low as Spot plus 36% for Silver Philharmonics.

Buy Gold Coins

GOLD PRICES (USD, GBP & EUR – AM/ PM LBMA Fix)

21-09-2022 1674.45 1671.75 1476.03 1474.65 1687.68 1687.13

20-09-2022 1667.90 1664.15 1458.75 1460.29 1665.56 1667.48

16-09-2022 1664.30 1664.65 1461.75 1460.06 1666.96 1668.65

15-09-2022 1689.00 1689.10 1467.23 1467.32 1690.01 1689.10

14-09-2022 1703.80 1703.90 1473.79 1473.70 1702.78 1706.97

13-09-2022 1727.05 1704.85 1474.38 1474.35 1699.94 1699.56

12-09-2022 1726.50 1726.40 1478.23 1477.28 1698.01 1705.51

09-09-2022 1726.95 1713.40 1485.87 1479.52 1711.58 1705.18

08-09-2022 1720.25 1709.35 1498.17 1488.33 1720.42 1716.19

07-09-2022 1705.05 1702.65 1486.63 1492.54 1722.10 1719.34

Buy gold coins and bars and store them in the safest vaults in Switzerland, London or Singapore with GoldCore.

Learn why Switzerland remains a safe-haven jurisdiction for owning precious metals. Access Our Most Popular Guide, the Essential Guide to Storing Gold in Switzerland here

Receive Our Award Winning Market Updates In Your Inbox – Sign Up Here